Since mid

June 2014 the price of oil fell almost 45%, with the spot price

for WTI in US$ 59.72 and Brent in US$ 63.64 on 12/11; while future oil prices points

on a strong downward trend.

Behind

these figures exists supply as well as demand factors. On the supply side,

according to IEA in October oil supply reached 94.2 mb/d, compared with 91.3

mb/d on 2013. The increase in oil supply has been driven by the US shale oil

revolution, Canadian tar sands, and increases in oil production among some OPEC

countries. The US increase in oil production, driven mainly from the fracking

and horizontal drilling revolution, allowed the country to increase its oil

production in more than 80% since 2008, reaching 9 mb/d in 2014. In OPEC,

stands out the rise, in the lasts months, in Libya oil production which, while

still showing signs of weakness, contributed partly to offset drops somewhere

else in OPEC, and help to have the group well above the 30 mb/d target.

On the demand side, the sluggish

world economy has moderated the increase in oil demand, and this is

complemented with a reduction on OECD oil consumption.

As a result of these trends, and the

OPEC decision on November 27 2014 to maintain its 30 mb/d target, supply has

shown a strong upside pressure than demand, which has had a tough downward

pressure on the oil price.

How long

will oil prices stay low, well that will depend on how tight become the

relation between demand and supply. OPEC has a spare capacity of about 3 mb/d;

almost 90% of it is in Saudi Arabia. Thus, a 1% supply disruption in any OPEC

and Non-OPEC can drive significant

pressure in the oil market. OPEC disruptions have not been an unusual thing, as

intended or unintended situations. There is no assurance that there will be no

more oil supply disruptions in Libya, Nigeria, Iran and Venezuela, as long

those countries continue experiencing geopolitical risks. Also, events of

nature or terrorist attacks can put an upward pressure in oil prices. Second,

with decreasing output from current wells and increasing global oil

consumption, there is the permanent need to add new production capacity. A 6% rate

of decline in oil production implies that 5.5 mb/d of new capacity are required

only to replace the lost production, and on top of that new additional capacity

is needed only to attend oil demand growth, which has grown in steps close to 1

mb/d. For shale oil wells, the rates of decline are much higher, and can go up

to 70% on average. Requiring an exploration and drilling effort much higher in

shale oil wells than in conventional oil wells. Given the higher depletion rate

of current shale oil wells, a fall in exploration and drilling will have a

faster downward adjustment in shale oil production. A sign in this direction is

observed in the fact that in October permits for new wells dropped 15 percent

across 12 major shale formation, according to industry data reported by

Reuters, what offers a sign of a slowdown in a drilling race that has seen

permits double since November 2013. Some drop of drama should be taken away

since a continual improvement in drilling and fracking technology is improving

shale oil wells productivity (super fracking technologies).

Thus, the

task to feed current world oil consumption is not an easy one and is subjected

to many events which can suddenly disrupt supply and skyrocket prices again,

and we will continuous seen events such as: political stress, war, lack of

spare capacity, financial and economic crisis, terrorist attack, OPEC cuts,

weather or nature events, and many others which severely reduce oil production

with figures as small as 1% of current consumption.

Source: Seadrill, Morgan Stanley Equity Research, International Energy

Agency

OPEC is a

very diverse club; some members are low cost producers with large wealth funds

that can finance fall in oil prices without having major fiscal troubles, while

others are high cost producers with not much money to confront the fiscal imbalances

that will face with a drop in the oil price. We should not be surprised if social unrest and geopolitical instability come up in some OPEC countries, contributing to an increased instability of oil supply. These differences make today much more difficult to reach an agreement within member countries. Where, at the end, and in the long term, what they have supported is the creation of new technologies that have enabled an efficient and competitive shale oil industry in the US. Thus, here, countries with clear advantages, in terms of their oil production costs and the strength of their economies, like the Saudis, find at best the decision to keep hands off.

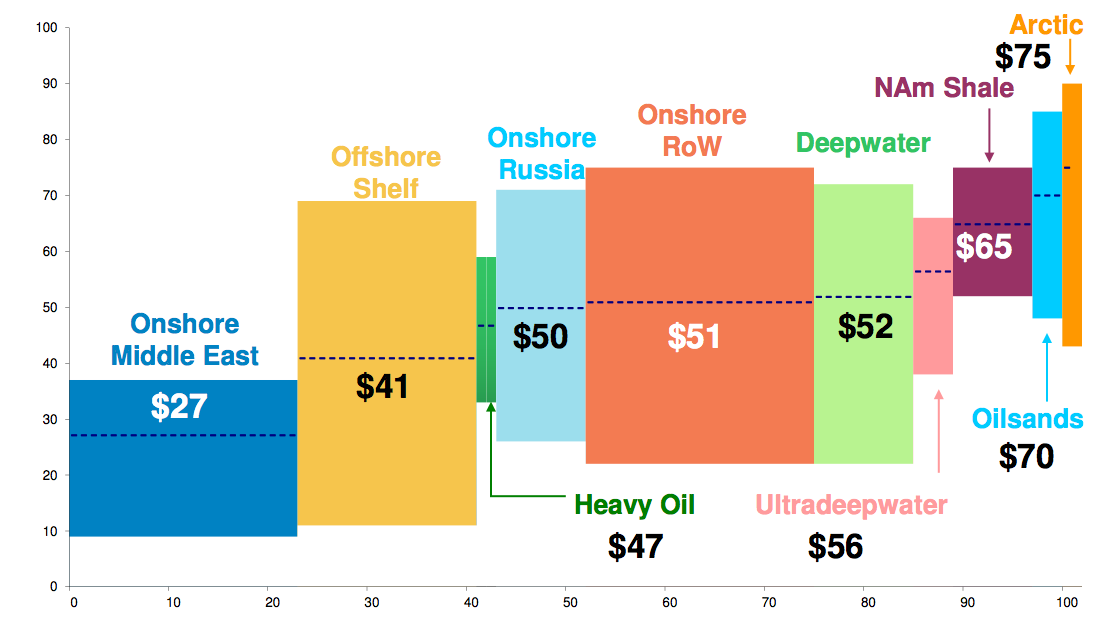

With the Saudis smart keep hands off policy in OPEC, as an intent to defend at least their market share, we might expect higher costs oil producer to exist the market, and the ones that are at the front line are ones with complex geologies, in remote areas, but of course those that set complex business environments for investors. In this race, how blessed a country has been with natural resources is only a part of the story. And, usually what is taking place over the ground is much more important for the success of the oil industry. What is clear at this moment is that the market is looking for a new equilibrium, and we should expect that oil prices will be more volatile in the short to medium term until high cost producers are out. Even though, the oil industry can always surprise as with mayor oil disruption that severely change market prices.

With the Saudis smart keep hands off policy in OPEC, as an intent to defend at least their market share, we might expect higher costs oil producer to exist the market, and the ones that are at the front line are ones with complex geologies, in remote areas, but of course those that set complex business environments for investors. In this race, how blessed a country has been with natural resources is only a part of the story. And, usually what is taking place over the ground is much more important for the success of the oil industry. What is clear at this moment is that the market is looking for a new equilibrium, and we should expect that oil prices will be more volatile in the short to medium term until high cost producers are out. Even though, the oil industry can always surprise as with mayor oil disruption that severely change market prices.